The sweeping Republican victory in US elections revived the American dream. President Trump would be a positive disruptive force for America. Active fiscal policy and tariffs would boost internal demand, and supply-side economics would provide funding and expand capacity. US macro would undoubtedly benefit, although perhaps at the cost of temporary higher inflation and interest rates. The rest of the world would bear the cost via weaker currency and US onshoring. America would be exceptional again.

The first two months of the new administration tell a different story. US macro policy is more focused on appeasing the electoral base than on generating growth. The lack of predictability generates uncertainty. The combination of the two subtracts from growth. Furthermore, midterm elections are still far away, and policy flexibility is limited. The bar for policy to support the economy is higher than the market thinks. We suspect an imminent growth scare is about to come that risk assets are not priced for.

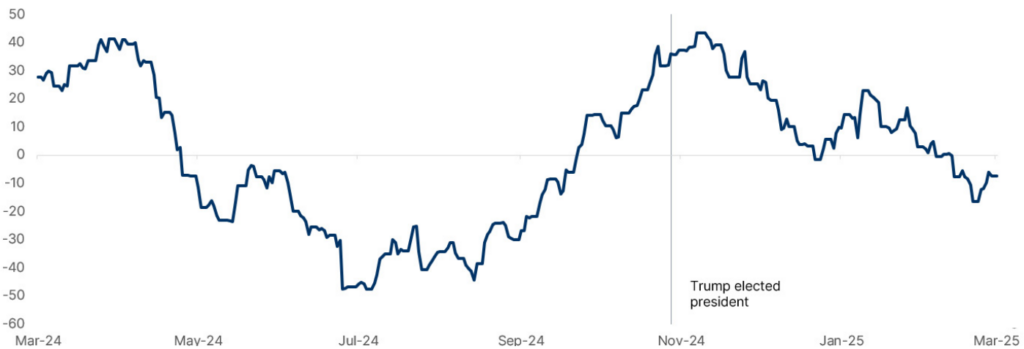

US economic data are deteriorating meaningfully. Jobless claims are on the rise, pushing non-farm payrolls to six-months low, and the unemployment rate above 4%. Economic surprises have been trending down steadily since November (Chart 1).

Source: Citi Bank, Bloomberg Finance LP, Algebris Investments. Data as of 07.03.2025. Note: Citi US Economic Surprise Index.

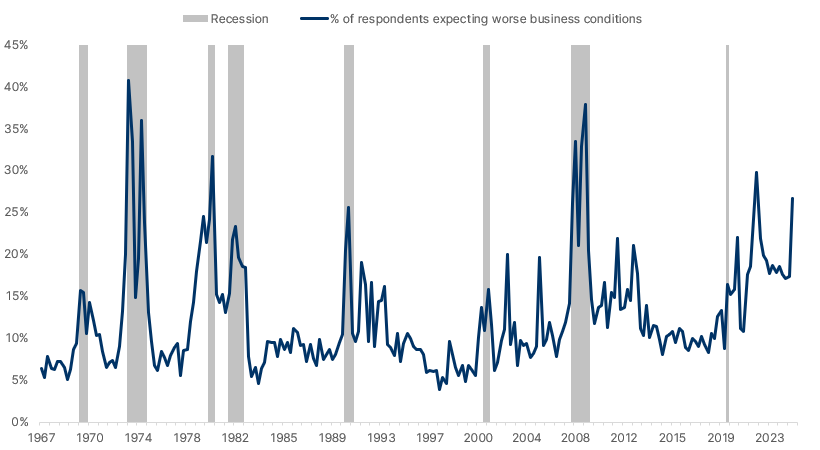

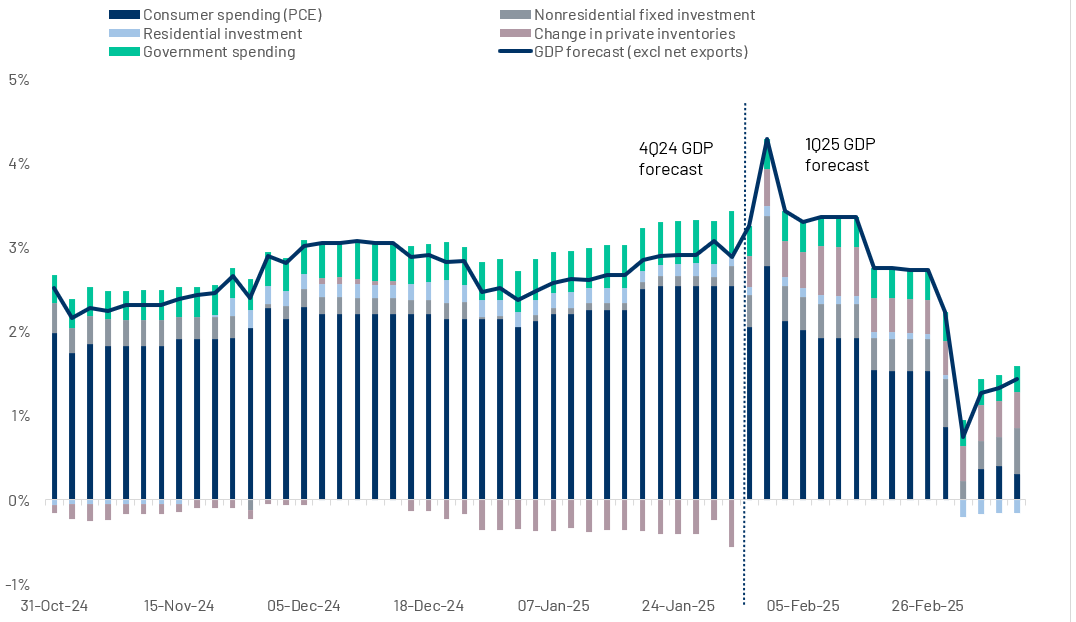

Consumer confidence, the key driver of the 2023-24 expansion, has deteriorated in 2025-to-date (Chart 2), driven by the perceived impact on business and labor market conditions. Real time gauges of US GDP are dropping sharply (Chart 3), driven by import surges but also by more tepid consumer spending.

Source: Conference Board. Data as of 07.03.2025.

Note: Consumer Confidence Next 6 Months. Pessimistic Expectations: Business Conditions..

Source: Atlanta Fed, as of 07.03.2025.

Note: Subcomponent Contributions to GDPNow 2024 4Q & 2025 Q1 Forecast excluding Net Exports component.

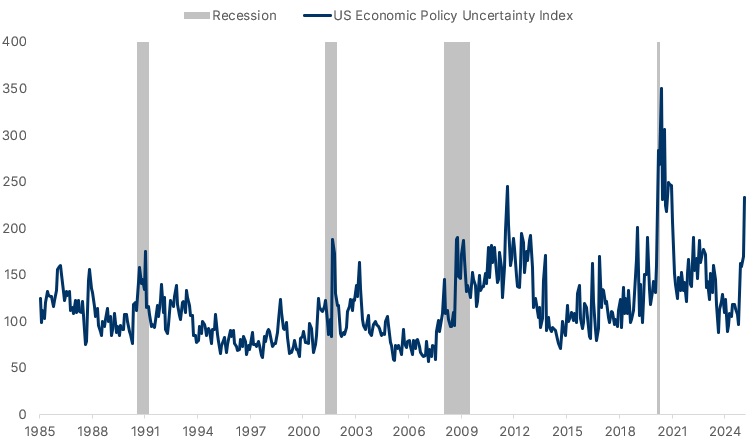

We suspect the US is currently undergoing a deep uncertainty shock. Evidence shows that policy uncertainty can be as bad for the cycle as an adverse exogenous shock. When uncertainty is too high, firms temporarily and suddenly pause investment and hiring. Output and employment tend to fall quickly as a result. US policy uncertainty is at the second highest level of the past forty years (Chart 4). Previous spikes were accompanied by a slowdown. Business surveys in January and February suggest sharp drops in new orders and employment.

Source: Baker, Scott R.; Bloom, Nick; Davis, Stephen J. Data as of 07.03.2025.

Note: US Economic Policy Uncertainty Index.

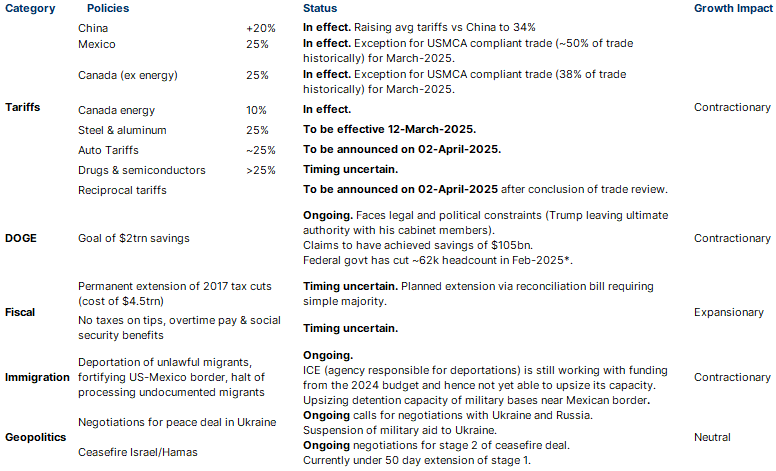

The first actual policy steps are not encouraging either. The administration is frontloading growth-unfriendly policies, such as job cuts in the public sector and trade restrictions (Table 1). The US tariff rate rose to 4% this year and may increase to 10-15% if and when fully implemented. Recent IMF research estimates the US growth drag from tariffs at 0.8% over one year. According to the plan, the bulk of growth expansion should be driven by tax cuts. These will take time to materialize as they have to go through Congress and funding remains a challenge.

Source: Veda Partners, Oxford Economics, Signum, The Guardian, Bloomberg LP. Data as of 08.03.2025.

Note: *the federal govt headcount cuts cannot be directly linked to DOGE initiatives.

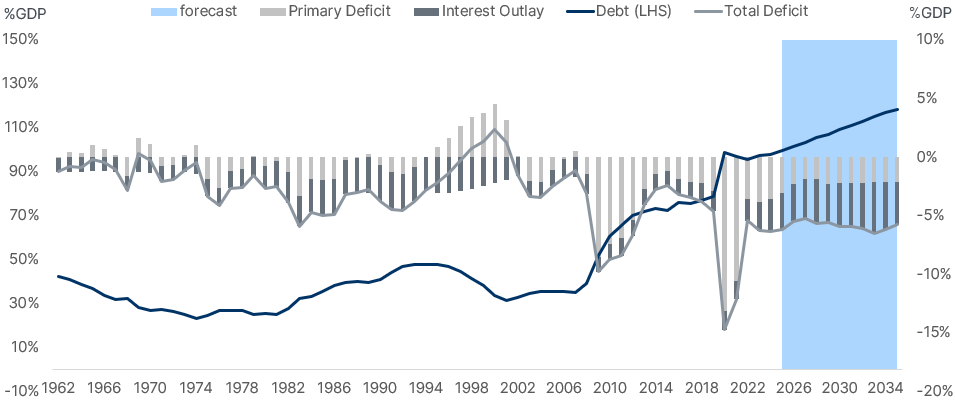

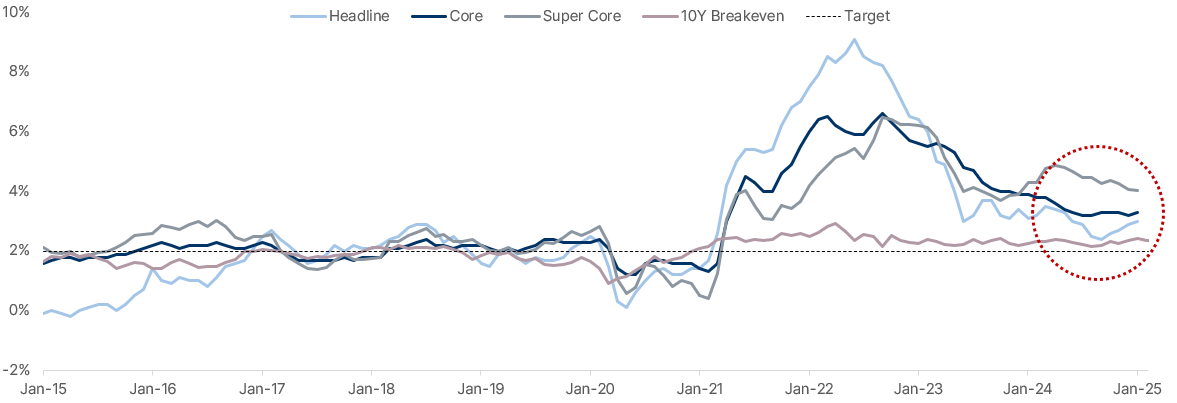

The cost of a US downturn is high as the policy space to respond to it is limited. US debt is high and bound to increase on a growth shock (Chart 5). Interest costs are just shy of 3% of GDP, leaving little space for primary spending. US inflation runs above target and stopped slowing in late 2023 (Chart 6). A trade-induced slowdown is not obviously deflationary, leaving the Fed in a tough spot. Secretary Bessent has stressed that the administration’s measure of success is more likely to be the price of ten-year Treasuries than the price of equity. President Trump has strengthened this message. This rhetoric aligns with a lack of urgency regarding supportive policy.

Source: CBO, Algebris Investments. Data as of 17.01.2025. Note: All metrics as % of GDP.

Source: Bloomberg Finance LP, Algebris Investments. Data as of 07.03.2025.

Note: Headline: US CPI Urban Consumers YoY NSA (CPI YOY Index), Core: US CPI Urban Consumers Less Food & Energy YoY NSA (CPI XYOY Index), Supercore: US Bloomberg BLS CPI Core Services Less Housing (Supercore) YoY (CSXHSPCY Index). US Breakeven 10 Year – USGGBE10 Index. Calculated by subtracting the real yield of the inflation linked maturity curve from the yield of the nominal Treasury maturity.

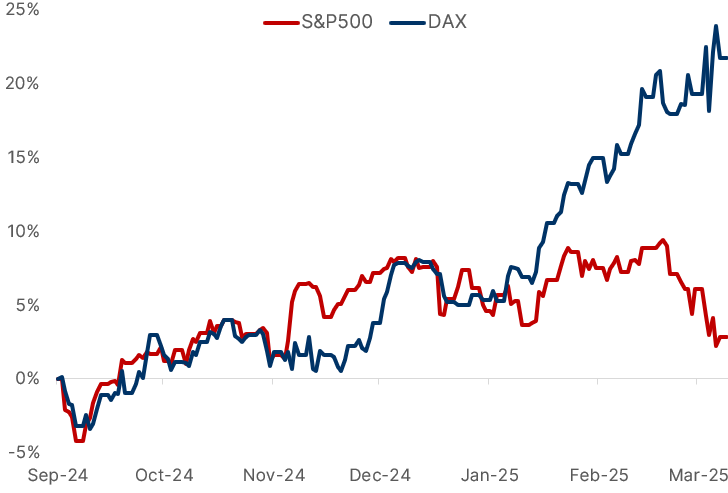

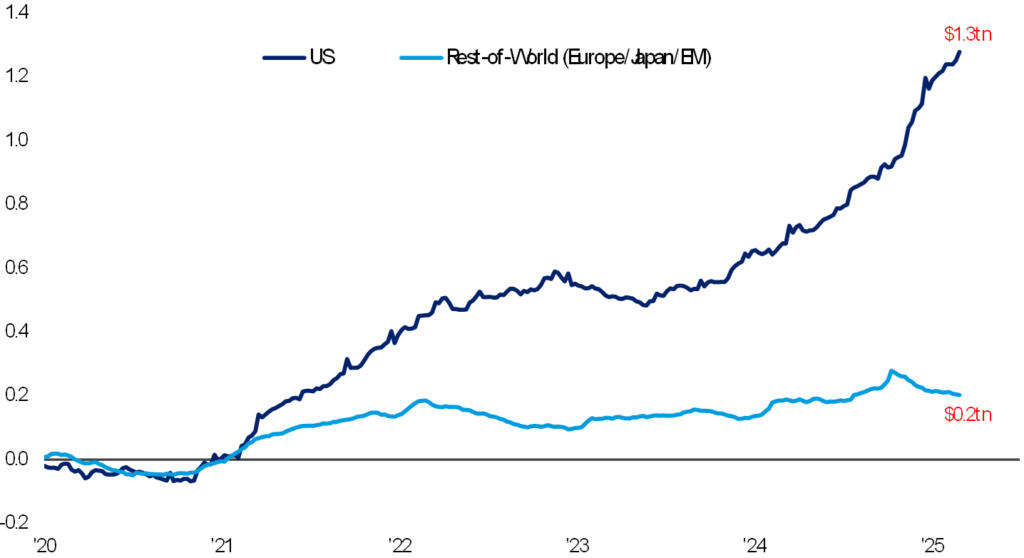

US exceptionalism is fading in the data, but well alive in markets. The S&P 500 trades at 23x, 15% above the ten year average. The US Dollar real exchange rate is at forty year highs, despite the US having grown slower than most of Asia for the past twenty years. Both trends are reverting fast (Charts 7 and 8), but multi-year indigestion of US assets suggests room for further correction.

Source: Bloomberg Finance LP, Algebris Investments. Data as of 07.03.2025.

Note: Local currency total returns of S&P 500 & DAX.

Source: Bloomberg Finance LP, Algebris Investments. Data as of 07.03.2025.

Note: US Dollar Index (DXY).

Risk assets have flourished recently, but large macro adjustments are in place in the United States. This may lead to a quick re-pricing of the winners of the past two years. We see US equities and the US Dollar most at risk. European assets are broadly under-owned, although enthusiasm about the new fiscal framework is boosting valuations. Credit is tight overall, but more attractive in selected sectors, particularly in Europe, as dispersion remains high. We see more value in US than European rates. EM credit is tight but value is emerging in local markets.

In the past three years, markets have come to terms with the idea of higher inflation and rates, but slowdowns have been forgotten. We see pre-conditions for one in 2025, with investors broadly unprepared. Volatility is on the rise, and active strategies are set to stand out.

Source: BofA Global Investment Strategy, EPFR, Algebris Investments. Data as of 10.03.2025.

Note: cumulative inflows into equity funds.

Davide Serra

Founder & CEO

Sebastiano Pirro

CIO & Financial Credit Portfolio Manager

Gabriele Foà

Global Credit Portfolio Manager

Silvia Merler

Head of ESG & Policy Research

Lennart Lengeling

Macro Analyst

For more information about Algebris and its products, or to be added to our distribution lists, please contact Investor Relations at algebrisIR@algebris.com. Visit Algebris Insights for past commentaries.

This document is issued by Algebris Investments. It is for private circulation only. The information contained in this document is strictly confidential and is only for the use of the person to whom it is sent. The information contained herein may not be reproduced, distributed or published by any recipient for any purpose without the prior written consent of Algebris Investments.

The information and opinions contained in this document are for background purposes only, do not purport to be full or complete and do not constitute investment advice. Algebris Investments is not hereby arranging or agreeing to arrange any transaction in any investment whatsoever or otherwise undertaking any activity requiring authorisation under the Financial Services and Markets Act 2000. This document does not constitute or form part of any offer to issue or sell, or any solicitation of an offer to subscribe or purchase, any investment nor shall it or the fact of its distribution form the basis of, or be relied on in connection with, any contract therefore.

No reliance may be placed for any purpose on the information and opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Algebris Investments, its members, employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions.

This document is being communicated by Algebris Investments only to persons to whom it may lawfully be issued under The Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 including persons who are authorised under the Financial Services and Markets Act 2000 of the United Kingdom (the “Act”), certain persons having professional experience in matters relating to investments, high net worth companies, high net worth unincorporated associations and partnerships, trustees of high value trusts and persons who qualify as certified sophisticated investors. This document is exempt from the prohibition in Section 21 of the Act on the communication by persons not authorised under the Act of invitations or inducements to engage in investment activity on the ground that it is being issued only to such types of person. This is a marketing document.

The distribution of this document may be restricted in certain jurisdictions. The above information is for general guidance only, and it is the responsibility of any person or persons in possession of this document to inform themselves of, and to observe, all applicable laws and regulations of any relevant jurisdiction. This document is suitable for professional investors only. Algebris Group comprises Algebris (UK) Limited, Algebris Investments (Ireland) Limited, Algebris Investments (US) Inc. Algebris Investments (Asia) Limited, Algebris Investments K.K. and other non-regulated companies such as special purposes vehicles, general partner entities and holding companies.

© 2025 Algebris Investments. Algebris Investments is the trading name for the Algebris Group.